The Eviota project aims to develop sustainability reports directly linked to

the financial accounts of companies, NGOs, and civil society organisations.

The initial phase focuses on estimating greenhouse gas emissions and air pollutants.

Our goal is to generate reliable, expenditure-based estimates of the carbon

and pollution footprint of music-related social enterprises—an approach we

refer to as connected financial and sustainability reporting.or

double materiality reporting.

Creating connected or double materiality reports has many advantages:

- It demonstrates to consumers, donors, and buyers that the organisation is committed to sustainable growth.

- It enables the organisation to apply for grants aimed at improving sustainability.

- Within the EU, it increases eligibility for green loans, green insurance, and green investments.

- Large corporations—including music event sponsors—may require credible sustainability metrics from their supply chain.

There are several challenges we aim to overcome in this project.

Connected financial and sustainability reports are complex, require extensive data, and are currently mandatory only for ’large’ corporations. Just as small enterprises

can file simplified tax returns and financial reports, we aim to create asimplified, low-cost, connected financial and sustainability report

for micro- and small organisations.Due to their complexity, these reports are time-consuming and expensive to produce.

The European Commission estimates the average cost at approximately €10,000 per organisation.We follow the

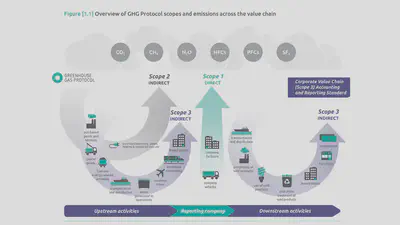

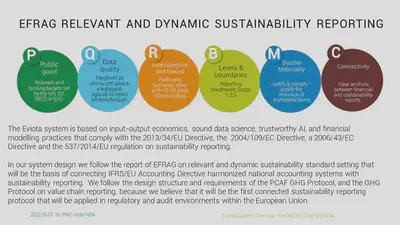

principle of double materiality, as defined by EFRAG and the CSRD.

This means our reports reflect both the organisation’s impact on society and the environment

(impact materiality), and the effects of sustainability risks on the organisation’s own financial health

(financial materiality). This dual perspective is essential for aligning sustainability information

with core financial disclosures.

In the European music sector, only a few large organisations are active. As a result, there is little regulatory pressure for music enterprises to engage in sustainability reporting—meaning they currently miss out on the associated benefits outlined above.

Table of Contents

Our approach

Most sustainability calculators are complex, relying on a wide range of data inputs from within the company. Our mission is to reduce this complexity—while maintaining accuracy—by identifying meaningful simplifications based on practical experience.

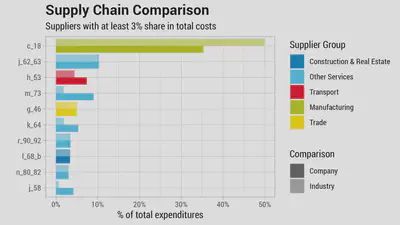

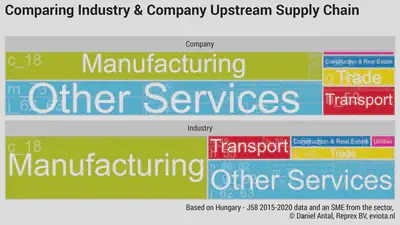

Rather than asking for dozens of indicators, we compare all spending (upstream supply chain) and all income (downstream value chain) with benchmark data from comparable organisations in the same country and sector for the reference year.

We offer free, manual calculation in the first phase to ensure we define these simplifications accurately. To reduce the time and effort required to collect data on your purchases and sales,

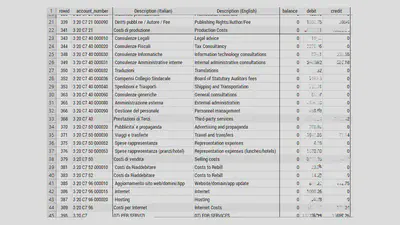

we rely on a component of standard bookkeeping: the trial balance.

The trial balance is an annual summary of general ledger accounts. For our purposes, we only require the revenue and expense accounts—not the full ledger, nor details on assets, liabilities, or capital gains/losses.

This information is readily available from your accountant and can typically be exported directly from your accounting software.

Why the trial balance?

We start from a document that every company has and that requires no additional management effort to prepare: the trial balance. This accounting report can be easily obtained from your accountant.

A trial balance lists the balances of all general ledger accounts at a specific point in time. It includes all major financial categories—assets, liabilities, equity, revenues, expenses, gains, and losses. Its primary function is to ensure that all debit and credit entries recorded in the general ledger are balanced.

No extra management time required: the trial balance is already generated by your accountant. We do not need the full ledger—only the annual summaries of revenues and expenses.

It is objective: the trial balance reflects actual spending, with no estimation or interpretation needed.

It is widely standardised: trial balances follow a fairly uniform structure across Europe and most countries globally (with the exception of the United States and a few others).

It ensures consistency: using the same source document as your accountant preserves the financial-sustainability connectivity principle. For example, if your financial report states that you spent €1,000 on energy, we will base our emissions calculation on the volume of energy corresponding to that amount, ensuring alignment between financial and environmental reporting.

This approach eliminates the need for excessive data entry into the calculator. At this stage, we do not offer an uploader, as we are manually testing different trial balances to validate our method before automating the upload process.

How does it work?

In future versions, the calculator will allow users to upload their trial balance to a secure location, answer a few basic questions, and receive a sustainability report in return. Because the format of trial balances varies depending on company size and national regulations, we need to conduct some manual processing to standardise inputs across cases.

We rely on the trial balance (see examples) because it is a standard accounting document held by all companies. It provides a clear overview of all purchases and sales, and requires no additional preparation from the organisation.

Currently, your accountant prepares two documents that are legally required and typically published together as your (Simplified) Annual Report. In Europe, all micro- and small enterprises produce this report, which consists of:

- The annual (simplified) balance sheet

- The annual (simplified) profit and loss statement

Using exactly the same underlying data—i.e. the trial balance—and adding sustainability information, we introduce a third document:

- The annual (simplified) sustainability report, which serves as a non-financial disclosure and complements the traditional financial statements.

Process: From your data to the final report

We sign a non-disclosure agreement.

You send us your trial balance.

We prepare a first draft of your carbon footprint. We categorise your suppliers (costs) and buyers (income) into 64 categories for which we have reliable environmental data. See our methodology below.

Most of our calculations are performed using iotables, our scientific, open-source software. We rely on open data from the Green Deal Data Observatory, which provides harmonised datasets from Eurostat and the European Environment Agency in readily usable formats. The use of open-source tools and open data helps keep our costs low.

We arrange a short call with you and your accountant to clarify any remaining details.

We deliver the final report.

What is the report?

The report is technically a non-financial disclosure (NFD) that complements your annual financial report, which currently includes the balance sheet and profit and loss statement. You may add a sustainability report as a third, optional component.

The creation of an NFD is not mandatory for small- and medium-sized enterprises (SMEs) and NGOs, which typically produce simplified financial reports.

The sustainability report consists of two paragraphs of factual text, accompanied by a table and a chart illustrating the greenhouse gas emissions (or other pollutants) associated with your organisation’s activities.

A sustainability report is an essential first step towards factual sustainability management and avoiding greenwashing. By understanding how your activities—including purchases from suppliers—generate emissions (or contribute to issues like the gender pay gap), you can plan to reduce negative impacts and enhance positive ones.

We collaborate with expert advisors to ensure that your actions and sustainability claims are credible. This enables you to communicate transparently and confidently with your customers, audience, donors, grant agencies, banks, insurers, or investors.

Why Eviota?

The first step in protecting our planet is to objectively identify where your organisation’s stakeholders—suppliers, buyers, workers, and technologies—leave an environmental footprint.

Methodology

We follow the CPA classification for categorising suppliers and corporate buyers. Some categories—such as

B MINING AND QUARRYING—are aggregated, meaning we cannot distinguish between specific mining activities. In service industries, this level of detail is not required.We use the same national accounts data as EU and UN institutions rely on to monitor compliance with the Paris Agreement. Our categories are based on the System of National Accounts (SNA), harmonised at EU and global level. In 2022, we worked with EU member states and candidate countries; the software will be adapted for global use in 2023 and beyond.

Our sustainability methodology is grounded in the Global GHG Accounting & Reporting Standard for the Financial Industry.

We follow EFRAG’s Proposals for a Relevant and Dynamic EU Sustainability Reporting Standard Setting (PDF download), which will underpin future mandatory sustainability reporting standards in Europe.

We support small music organisations with sustainability reporting—particularly where detailed data or standards currently exist only for greenhouse gas emissions.

The Music Eviota project is supported by MusicAIRE.

Open collaboration

Our project is rooted in open collaboration. The MusicAIRE grant provides us with resources to support additional music businesses, civil society organisations, and researchers with high-quality data—free of charge during the project’s duration.

We actively welcome collaboration from those interested in applying our data and research in real-world policy, sustainability reporting, or business development. Testing and validating our models in practical contexts will help us improve their usability and long-term value.

Why are we developing this service?

The European Green Deal, including the proposed Corporate Sustainability Reporting Directive (CSRD), and the broader sustainable finance package, aims to set the European economy on a permanent path towards decarbonisation and increased sustainability. This includes reforms to how economic activities are financed—through bank loans, insurance, investment, and direct subsidies.

From 2023 onwards, organisations that can demonstrate alignment with environmental, social, and governance (ESG) principles, as outlined in the Paris Agreement and supported by UN, OECD, and EU frameworks, will gain easier and more affordable access to finance.

Correct and reliable sustainability management will offer financial advantages, but also greater responsibility. The European Financial Reporting Advisory Board (EFRAG) is developing a unified standard for financial and sustainability reporting. This standard will be used across the financial services industry and large companies throughout Europe’s supply chains. The European Commission estimates compliance costs up to the end of 2023 at €4 billion, with reporting and auditing expenses reaching €10,000 per organisation.

While music-sector MSMEs (micro, small, and medium-sized enterprises) and civil society organisations (CSOs) will be exempt from mandatory sustainability reporting,

they can still benefit from voluntary compliance and credible reporting. Our solution provides tangible benefits for music MSMEs and CSOs:

A size-appropriate tool for sustainability management and reporting—starting with greenhouse gas emissions, and expanding to water usage, pollution, biodiversity, and recycling across the full value chain. For example, it can flag environmental risks in a festival’s supplier base (e.g., transport, catering, security).

Extendibility to social sustainability. Our prior research shows that live music, which relies on a large workforce, often suffers from underrepresentation and discrimination against women in technical and managerial roles. Our system can flag risks such as gender pay gaps and provide benchmarks for internal improvements.

Our review of ESG risk management confirms that compliance is not only useful for securing better loan and insurance terms (particularly relevant for live events), but is also increasingly expected by event sponsors and audiences.

While some music organisations already publish sustainability reports, these are often unstandardised and disconnected from financial data. Our approach adds credibility by integrating sustainability data into the same framework used for financial reporting—providing elective but trustworthy non-financial disclosures for MSMEs.

Future plans: Social Sustainability and Anti-Bribary

MusicAIRE Green Recovery in the Music Sector

The objective of the MusicAIRE GREEN Recovery Programme is to increase environmental sustainability and ecological awareness within the music sector. Its focus is on greening the industry—particularly live performances, festivals, and touring—while also supporting innovative start-ups that seek to reduce the environmental impact of online data storage and music distribution.

Reprex

Big data for all

Reprex is a Netherlands-based AI company that builds data-sharing spaces and knowledge bases to deliver trustworthy, explainable, and human-controlled AI.

MusicAIRE

MusicAIRE is an EU-funded project that will contribute to the recovery of the music ecosystem.